(Updated July 7, 2021)

Paycheck Protection Program Update

The Paycheck Protection Program ended on May 31, 2021. Carson Community Bank was one of the few minority depository institutions that was allowed access to continue to submit PPP loan applications through the deadline. Over the past year our team submitted over 950 PPP loans which secured over $16 million in funding for our local communities.

2021 PPP Loans and What to Expect

Given the volume of loans our team produced this year, and to maximize the chance that the entire PPP loan will be forgiven, we are using the 24 week covered period to start the forgiveness application process. Our team is monitoring when the 24 week covered period has expired for your loan.

- Some time after the 24 week covered period is complete, a loan officer will reach out to you to start the forgiveness process. You do not need to contact our team until we reach out following the completed 24 week covered period.

- Depending on the type of loan (contractor/sole proprietor, C-Corp, S-Corp, Partnership, Non-profit, etc) and loan amount, your loan officer will help guide you through the process.

- We are utilizing software called Abrigo to help the efficiency of processing forgiveness applications, so once your 24 week period is complete keep an eye out for Adobe Sign (echosign@echosign.com).

How to Prepare

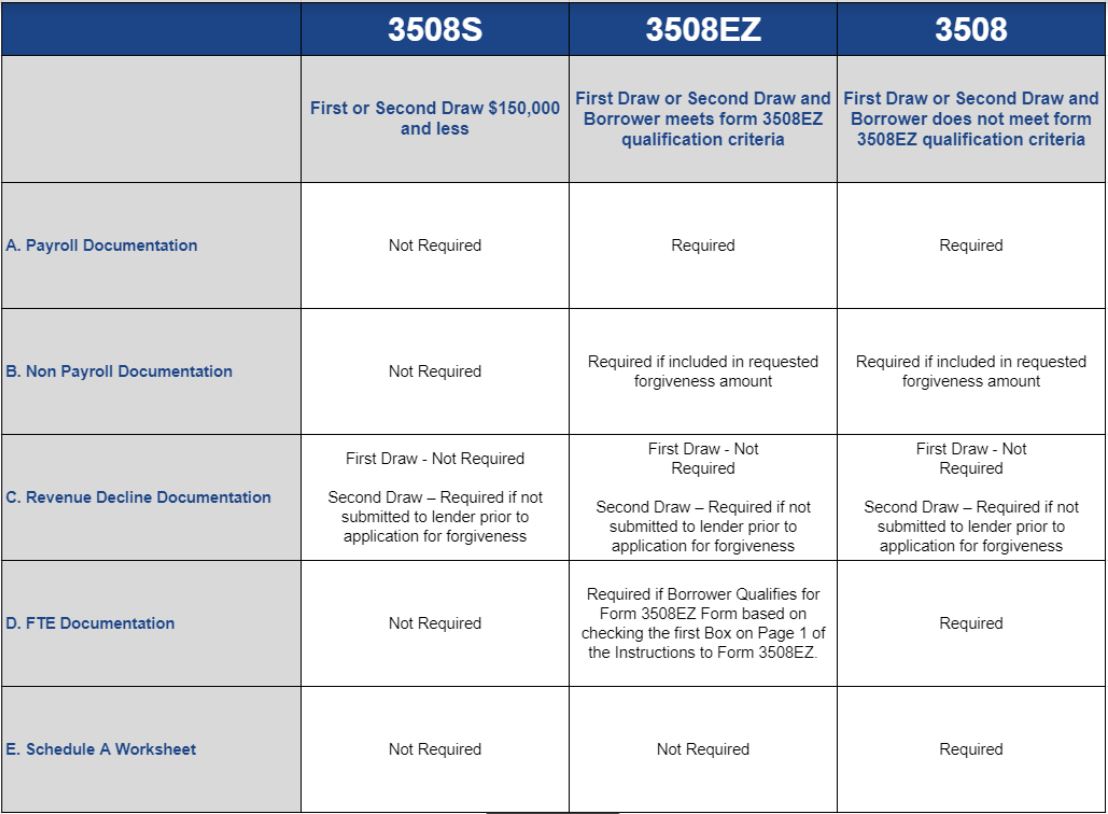

Below is a chart on the documents required based on your PPP loan type and amount.

How do I know which forgiveness form to use?

- Form 3508S - this form is for borrowers who took out loans of $150,000 or less.

- Form 3508EZ - this form is for borrowers who did not reduce employee levels, wages, or hours.

- Form 3508 - this form is for all other borrowers who do not qualify for the 3508S or 3508EZ.

Below is a further explanation of the required documentation. Please read the applicable Loan Forgiveness Application and Instructions in full to ensure you understand all the documents that are required to be submitted and maintained in connection with your Loan Forgiveness Application.

Documentation verifying the eligible cash compensation and non-cash benefit payments from the Covered Period or the Alternative Payroll Covered Period consisting of each of the following:

- Bank account statements or third-party payroll service provider reports documenting the amount of cash compensation paid to employees.

- Tax forms (or equivalent third-party payroll service provider reports) for the periods that overlap with the Covered Period or the Alternative Payroll Covered Period:

-

- Payroll tax filings reported, or that will be reported, to the IRS (typically, Form 941).

-AND-

-

- State quarterly business and individual employee wage reporting and unemployment insurance tax filings reported, or that will be reported, to the relevant state.

- Payment receipts, cancelled checks, or account statements documenting the amount of any employer contributions to employee group health, life, disability, vision or dental insurance and retirement plans that the Borrower included in the Requested Loan Forgiveness Amount.

Other Payroll Documentation Requested by Carson Community Bank:

- Internal payroll reports for the Covered Period or the Alternative Payroll Covered Period where a recognized 3rd party payroll provider report is unavailable.

B. Non Payroll Documentation (If included in requested forgiveness amount)

- Business Mortgage Interest Payments

-

- Copy of lender amortization schedule and receipts or cancelled checks verifying eligible payments from the Covered Period or Lender account statements from February 2020 and the months of the Covered Period through one month after the end of the Covered Period verifying interest amounts and eligible expenses.

- Business Rent or Lease

-

- Copy of the Current Lease agreement and receipts or canceled checks verifying eligible payments from the Covered Period or lessor account statements from February 2020 and for Covered Period through one month after the end of the Covered Period verifying interest amounts and eligible expenses.

- Business Utility Payments

-

- Copy of invoices from February 2020 and those paid during the Covered Period and receipts, cancelled checks, or account statements verifying those eligible payments.

- Covered operations expenditures

-

- Copy of invoices, orders, or purchase orders paid during the Covered Period and receipts, cancelled checks, or account statements verifying those eligible payments.

- Covered property damage costs

-

- Copy of invoices, orders, or purchase orders paid during the Covered Period and receipts, cancelled checks, or account statements verifying those eligible payments, and documentation that the costs were related to property damage and vandalism or looting due to public disturbances that occurred during 2020 and such costs were not covered by insurance or other compensation.

- Covered supplier costs

-

- Copy of contracts, orders, or purchase orders in effect at any time before the Covered Period (except for perishable goods), copy of invoices, orders, or purchase orders paid during the Covered Period and receipts, cancelled checks, or account statements verifying those eligible payments.

- Covered worker protection expenditures

-

- Copy of invoices, orders, or purchase orders paid during the Covered Period and receipts, cancelled checks, or account statements verifying those eligible payments, and documentation that the expenditures were used by the Borrower to comply with applicable COVID-19 guidance during the Covered Period.

Note: For categories 1, 2 and 3 above, in addition to the information requested above, the Borrower must provide documentation verifying existence of the obligations/services prior to February 15, 2020.

C. Revenue Decline Documentation

For Second Draw Loans of $150,000 and less:

If the forgiveness application is being submitted for a Second Draw PPP Loan, the Borrower must submit documentation supporting the gross receipts reduction certification on the Borrower’s loan application (if the Borrower did not previously submit such documentation to the lender).

-

- Third Party Audited Income Statement for 2020 Quarter (If the financial statements are not audited, the Applicant must sign and date the first page of the financial statement and initial all other pages, attesting to their accuracy. If the financial statements do not specifically identify the line item(s) that constitute gross receipts, the Applicant must annotate which line item(s) constitute gross receipts.); and

- Third Party Audited Income Statement for 2019 Reference Quarter (If the financial statements are not audited, the Applicant must sign and date the first page of the financial statement and initial all other pages, attesting to their accuracy. If the financial statements do not specifically identify the line item(s) that constitute gross receipts, the Applicant must annotate which line item(s) constitute gross receipts.).

-OR-

-

- 2020 Tax Return or Schedule C (If the entity has not yet filed a tax return for 2020, the Applicant must fill out the return forms, compute the relevant gross receipts value, and sign and date the return, attesting that the values that enter into the gross receipts computation are the same values that will be filed on the entity’s tax return.); and

- 2019 Tax Return or Schedule C.

D. FTE Documentation (Only for Applicants using Form 3508, and Form 3508EZ in limited circumstances*)

Clients who are eligible to apply and are filing the 3508 application will also need to submit documentation showing one of the following:

-

- Documentation showing the average number of FTE employees on payroll per week employed by the Borrower between February 15, 2019 and June 30, 2019

-OR-

-

- the average number of FTE employees on payroll per week employed by the Borrower between January 1, 2020 and February 29, 2020

-OR-

-

- In the case of a seasonal employer, documentation showing the average number of FTE employees on payroll per week employed by the Borrower between February 15, 2019 and June 30, 2019; between January 1, 2020 and February 29, 2020; or any consecutive 12-week period between May 1, 2019 and September 15, 2019.

* Form 3508EZ applicants must provide FTE documentation when they check only the first Box on Page 1 of the Instructions to 3508EZ in order to qualify to use Form 3508EZ. See page 4 of Form 3508EZ for further details.

E. Schedule A Worksheet (Only for Form 3508 Applicants)

-

- Provide copy of Schedule A Worksheet

Note: Evolving SBA Forgiveness rules and guidelines may require additional information. For the most up to date guidelines on PPP Loan Forgiveness please visit the SBA website directly.

Document Retention

What documents do I need to retain for PPP loan forgiveness?

Funding for the PPP loan and loan forgiveness is based on funds used for payroll, interest, rent, and utility payments. In general, the items to maintain include:

- Loan application items: Retain all records submitted with the loan application.

- Loan necessity items: Retain all documents that support your necessity for the loan. Also, retain all documents that support your eligibility for the loan.

- Loan forgiveness application: Retain all documents that support your loan forgiveness application.

- Payroll records: Retain your business payroll registers and proof of fund transfers to fund the payroll. If you utilize a professional employer organization (PEO) to process your payroll, be sure to save your payroll invoice. This payroll invoice or report identifies payroll costs and employee benefits paid during the period used for loan forgiveness. Most payroll providers have created custom reports that pull the relevant payroll data that aligns with the loan forgiveness period.

- Utility bills: Keep invoices and statements for electric, gas, phone, internet, and heating service providers.

- Rent and mortgage interest statements: Keep proof of payments for any monthly rent and mortgage interest payments during the loan forgiveness period.

- Bank statements: Keep your bank statements that show outgoing payments related to the above items.

(Updated April 5, 2021)

Paycheck Protection Program Update

On March 30, President Joe Biden signed the PPP Extension Act of 2021 into law, extending the Paycheck Protection Program an additional two months to May 31, 2021, and then providing an additional 30-day period for the SBA to process applications that are still pending.

(Updated March 15, 2021)

Paycheck Protection Program Update

The Paycheck Protection Program ends on March 31, 2021. The deadline to contact one of our loan officers is March 19. If you did not previously qualify, you may now qualify given the latest guidance. The PPP rules are always changing, and we encourage you to review the latest SBA and Treasury PPP Re-Opening and New Guidance information to better understand the details.

New Schedule C Guidance

The key provisions in the new interim final rule, as of 3/4/21, include the following:

- A revised loan calculation formula for Form 1040, Schedule C sole proprietors, independent contractors, and self-employed individuals using gross income instead of net income.

- The rule provides guidance on how the calculation for borrowers in two ways: those with no employees and those with employees.

- Schedule C filers using gross income to calculate loan amounts with more than $150,000 in gross income will not automatically be deemed to have made the statutorily required certification concerning the necessity of the loan request in good faith. These borrowers may be subject to a review by SBA of their certifications.

- The rule also sets aside $1 billion for PPP loans to businesses in this category that do not have employees and are located in low- or moderate-income areas.

- It eliminates qualifying restrictions for small-business owners delinquent on their federal student loans or with prior non-fraud felony convictions.

- Non-citizen small-business owners who are lawful U.S. residents may use Individual Taxpayer Identification Numbers to apply for relief.

- The higher loan amounts for Schedule C borrowers apply to applications filed after the rule’s effective date. Loan amounts cannot be increased once the loan is disbursed to the borrower, so lenders and borrowers may wish to cancel loans that have not yet been disbursed and reapply using the new Schedule C application form.

Second Draw PPP Loans

If you applied for a first draw loan in 2021, you may be eligible to apply for a second draw loan. To qualify for a second draw loan you must meet the criteria listed below. We are recommending customers provide 2019 and 2020 quarterly gross income to ensure your application is processed timely.

Second Draw Eligibility

- you have no more than 300 employees, and

- you have experienced a greater than 25% reduction in gross receipts during the first, second, third, or fourth quarter in 2020 relative to the same quarter in 2019. You may also show an annual loss of 25%.

(Updated January 13, 2021)

Paycheck Protection Program Update

As part of the 2020 end-of-year pandemic relief package, Congress has passed several changes to the Paycheck Protection Program (PPP) and created a “Second Draw” PPP for small businesses who have exhausted their initial loan. Other changes impact eligibility for initial PPP loans, the loan forgiveness process, and the tax treatment of PPP loans.

If you are interested in applying for the SBA Paycheck Protection Program, please email us at sba@carsoncommunity.bank or contact your loan officer.

Getting Started

- You are a business with less than 300 employees.

- This is your first PPP loan OR you have used the full amount of your initial PPP loan on eligible expenses.

- You demonstrate a 25% reduction in gross receipts in any quarter of 2020 relative to the same quarter of 2019.

- Email sba@carsoncommunity.bank or contact your loan officer to state your interest.

Frequently Asked Questions

1. How Do New Changes Impact My Existing PPP Loan?

Tax Treatment: The new law overturns the IRS ruling and provides that regular business expenses paid for with PPP loan proceeds shall be deductible for tax purposes (applies to past and future loans).

Expanded List of Expenses Qualifying for Forgiveness: The list of expenses that PPP funds can be used for that qualify for loan forgiveness has been expanded to include:

- “operations expenses” defined as payments for business software and cloud computing services and other human resources and accounting needs that facilitate business operations;

- “supplier costs” defined as payments to a supplier for goods that are essential to the operations of the borrower pursuant to a contract or purchase order in effect before the PPP loan is disbursed or with respect to perishable goods, in effect at any time;

- “worker protection expenses” defined as operating or capital expenditures to comply with public health guidance related to COVID-19, including things like drive-through windows and sneeze guards and the purchase of personal protective equipment (PPE); and

- “covered property damage costs” defined as costs related to property damage or looting due to public disturbances in 2020 that are not covered by insurance or other compensation.

Remember: It is still the case that not more than 40% of the forgiven amount can be for non-payroll costs, which may limit how much of your loan can be forgiven.

Loan Forgiveness Reduction: If you also received an EIDL grant, your PPP loan forgiveness will no longer be reduced by the amount of the grant.

Loan Forgiveness Period: The period for which expenses count toward loan forgiveness will begin on the date of loan origination and end on a date of your choosing that is between 8 and 24 weeks after origination.

Simplified Application: If your loan was for less than $150,000, there will be a simplified one-page application process for loan forgiveness.

2. I Exhausted My Initial PPP Loan, How Does This Help Me?

The brand new “Second Draw” program is for small businesses, non-profits, sole proprietors, and independent contractors who have exhausted their initial PPP loan. The program will make new loans through March 31, 2021, or until the new funding is exhausted.

Eligibility: You are eligible for a second draw loan if you have exhausted your first PPP loan and

- you have no more than 300 employees, and

- you have experienced a greater than 25% reduction in gross receipts during the first, second, third, or fourth quarter in 2020 relative to the same quarter in 2019.

Loan Amount: The maximum loan amount is the average monthly payroll costs for the entity during the 12 months prior to the loan or, at the election of the borrower, 2019 multiplied by 2.5 (or 3.5 for employers in the accommodation and food service industry).

Seasonal employers utilize average monthly payroll costs for a 12-week period between February 15, 2019 and February 15, 2020.

A loan may not exceed $2 million.

Loan Forgiveness: The amount of loan that can be forgiven is the lesser of:

- Costs incurred or expenditures made between the date of the origination of the loan and ending on a date of your choosing that is between 8 and 24 weeks after origination for: (a) payroll costs, (b) qualifying mortgage interest or rent obligations, (c) covered utility costs, (d) covered operations costs, (e) covered property damage, (f) covered supplier costs, and (g) covered worker protection expenditures; or

- Payroll costs for the same period divided by 0.60 (this serves as a cap on the total loan forgiveness to ensure that at least 60% of the total amount forgiven is for payroll costs).

Like original PPP loans, the amount of loan forgiveness can be reduced if the borrower has (1) reduced the number of employees or (2) employee salaries by more than 25%. However, the same safe harbors that apply to original PPP loans apply to Second Draw loans.

3. What If I Never Received a PPP Loan?

For new PPP applicants, the loan process will largely remain the same with a few major changes:

- The PPP program is open through March 31, 2021, or until the new funding is exhausted.

- If you are a 501(c)(6), a local news media organization, or a housing cooperative you may be newly eligible for a loan.

- You may qualify even if you took advantage of the Employee Retention Tax Credit.

- If you are a publicly traded company, you are now prohibited from receiving a loan.

- Group insurance payment can be included in your payroll costs when determining your maximum loan amount.

- If you are a seasonal employer, you have greater flexibility in picking the 12-week period between February 15, 2019 and February 15, 2020 used to determine your payroll costs and thus your maximum loan amount.

New borrowers have until the end of the covered period of their loan (up to 24 weeks after origination) to restore a reduction in their number of employees or reduced wages in order to avoid having their loan forgiveness reduced. Note: The safe harbors for when an employer cannot find qualified employees or where complying with COVID related safety measures prevents a return to February 2020 levels of business activity and staffing remain in effect.

(Updated June 2020)

So you have a PPP loan –

What is next?

How to Get Your Loan Forgiven

The single largest advantage of the PPP program is the ability to have your loan forgiven so you are not obligated to make interest or principal payments. This will require following the rules of the Program and providing good records proving that you have followed those rules.

To have your loan forgiven either in total or in part, you must meet the following rules:

- Covered Period: Starting from the day you received the funds of the loan from Carson Community Bank, borrowers who received loans prior to June 5, 2020, can elect to use the funds to maintain or restore hiring over an 8 week period or a 24 week period. The advantage of the 8 week period is that it allows borrowers to receive their forgiveness faster, while the 24 week period allows for a longer time to achieve forgiveness. If the 24 week period is chosen, borrowers must maintain staffing levels for the entire period and only expenses up to December 31, 2020, can be included.

- 60% to Payroll: At least 60% of your loan proceeds must be used to pay for payroll costs. Payments to independent contractors CANNOT be included in your payroll cost. You can use the remaining loan proceeds (up to 40%) to pay eligible expenses such as mortgage interest, rent, and utilities.

- Headcount: The most important part of forgiveness is to maintain your staffing levels. To understand how much you need to spend on payroll to achieve forgiveness, calculate the average number of full-time equivalent (FTE) employees by using the following calculation:

• Calculate the average number of employees during the Covered Period (Either the 8 or 24 week period) following the date at which you obtained your loan proceeds. Call this “Base Amount”

• Calculate the number of FTE employees you had between February 15, 2019, and June 30, 2019. Call this “Option 1.”

• Calculate the number of FTE employees you had between January 1, 2020, and February 29, 2020. Call this “Option 2.” - Base Amount: Take the Base Amount and divide by Option 1 then do the same by dividing by Option 2. Take the largest number between your Option 1 and Option 2 calculation. Also note that if you are a seasonal employer, you must use Option 1. Note that borrowers can adjust option for FTE safe harbor exemptions (see below).

• If the result of your calculation is larger than “1,” then you successfully maintained your headcount, and you meet this requirement in full.

• If you get a number smaller than “1,” then you did not maintain your original headcount and the amount for which the PPP loan can be forgiven will be reduced proportionately. For example, if your calculation resulted in a “0.75” result, then you could be eligible for getting up to 75% of your loan forgiven provided you meet the other criteria. - Salary/Wage Amount: For every employee who did not make more than $100,000 of annualized pay for 2019, you must maintain 75% of the pay received during the 8 week test period compared to the most recent quarter they were employed. If pay was reduced below 75% compared to the quarter prior to the 8 week test period, then forgiveness will be reduced by that difference. For example, if you reduced pay by 50%, then 75% – 50% equals a reduction of forgiveness by 25%.

- Rehiring: If you furloughed, laid off, or terminated staff prior to the 8 week test period, you can hire them back on prior to June 30th, 2020 to still qualify for all or a portion of forgiveness. Further, if you reduced salary below the 75% level, you can also reinstate any pay below that level. If the employee rejects your reinstatement offer, borrowers may be allowed to exclude this employee when calculating forgiveness. To qualify for this exemption, you must:

• Make a written offer to rehire in good faith;

• Have offered to rehire for the same salary/wage and the number of hours as before they were furloughed or laid off; and,

• Receive a rejection by the former employee in writing. - Other “Safe Harbor” Employee Exemptions: In addition to the above, borrowers can also qualify for an exemption for the sake of payroll calculation if an employee was fired for cause, voluntarily resigned or voluntarily requested a reduction in his or her hours. Borrowers may also be required to demonstrate that they were unable to hire similarly qualified employees for unfilled positions, or document that due to safety requirements, borrowers were unable to return to normal operating levels. It should also be noted that any employee who rejects an offer for re-employment may no longer be eligible for continued unemployment benefits.

The Forgiveness EZ Form

On June 16, 2020, the SBA issued a simplified PPP Loan Forgiveness Application called the 3508EZ Form. This “EZ Form” is designed to reduce the required calculations for those who qualify. To qualify, borrowers must:

- be self-employed AND have no other employees; OR

- NOT have reduced salaries or wages of their employees by more than 25%, and must not have reduced the number of hours of their employees; OR

- have suffered a reduction of business activity as a result of health directives related to the COVID-19 pandemic and did not reduce salaries or wages of employees by more than 25%.

If you do not qualify under one of the three criteria, you must use the standard Forgiveness form called the “3508 Form”.

To see the current form and instructions, please go here:

https://home.treasury.gov/system/files/136/PPP-Loan-Forgiveness-Application-Form-EZ-Instructions.pdf

https://home.treasury.gov/system/files/136/PPP-Forgiveness-Application-3508EZ.pdf

The Documents You Will Need for Forgiveness

Once the Forgiveness period is open, you will need documents verifying the number of full-time equivalent employees on payroll and their pay rates, for the periods used to verify you met the staffing and pay requirements. These documents can be one or more of the following:

- Payroll reports from your payroll provider.

- 2019 Payroll tax filings (Form 941)

- Bank account statements showing qualified payroll, mortgage/lease payments or utility expenses.

- Schedule of employees to include their name, employee number, and compensation

- Income, payroll, and unemployment insurance filings from your state

- Documents verifying any retirement and health insurance contributions

- Documents verifying your eligible interest, rent, and utility payments (canceled checks, payment receipts, account statements) if these are being claimed.

- Documents evidencing any FTE safe harbor exemptions – written evidence that previous positions were offered and declined, were fired for cause, voluntarily resigned, or voluntarily requested a reduction in hours. In all cases, the borrower only has to potentially show written evidence if the position was not filled by another employee and forgiveness is being sought.

- If applicable, EIDL Advance amount and application number.

Note – If these documents are not in digital form, please take the time soon to scan these and get them ready for upload using an Adobe PDF, JPEG, or PNG file format. Please note that you can take a high-quality picture of the document and then upload the photo.

Documents that Borrower Must Maintain but Are Not Required to Upload

The following documents should be kept for six years after the loan is forgiven or repaid in the event the Office of the Inspector General, Bank, SBA, IRS, or other entity needs to review

- Compensation: Documentation (payroll records, staffing schedules, etc.) supporting the certification that annual salaries or hourly wages were not reduced by more than 25 percent during the Covered Period or the Alternative Payroll Covered Period relative to the period between January 1, 2020 and March 31, 2020.

- FTE and Hours: If applicable, documentation supporting that the Borrower did not reduce the number of employees or the average paid hours of employees between January 1, 2020 and the end of the Covered Period (other than any reductions that arose from an inability to rehire individuals who were employees on February 15, 2020, if the Borrower was unable to hire similarly qualified employees for unfilled positions on or before December 31, 2020). This documentation must include payroll records that separately list each employee and show the amounts paid to each employee between January 1, 2020 and the end of the Covered Period.

- Safe Harbor Employees: Documentation regarding any job offers and refusals, refusals to accept restoration of reductions in hours, firings for cause, voluntary resignations, written requests by any employee for reductions in work schedule, and any inability to hire similarly qualified employees for unfilled positions on or before December 31, 2020.

- Operations: If applicable, documentation supporting that the Borrower was unable to operate between February 15, 2020 and the end of the Covered Period at the same level of business activity as before February 15, 2020 due to compliance with requirements established or guidance issued between March 1, 2020 and December 31, 2020 by the Secretary of Health and Human Services, the Director of the Centers for Disease Control and Prevention, or the Occupational Safety and Health Administration, related to the maintenance of standards of sanitation, social distancing, or any other work or customer safety requirement related to COVID-19. This documentation must include copies of the applicable requirements for each borrower location and relevant borrower financial records.

- Other Supporting Materials: Borrowers should retain all worksheets, calculations, schedule or other records relating to the Borrower’s PPP loan, including documentation submitted with its PPP loan application, documentation supporting the Borrower’s certifications as to the necessity of the loan request and its eligibility for a PPP loan, documentation necessary to support the Borrower’s loan forgiveness application, and documentation demonstrating the Borrower’s material compliance with PPP requirements

Loan Forgiveness Details and Limits

- Self-Employed: Borrowers who are self-employed are entitled to use PPP funds to replace lost compensation due to the impacts of COVID-19. It is important to note, however, that borrowers are not entitled to use the full amount of the loan to replace pay. Only 8 weeks’ worth of a borrower’s 2019 net profit is eligible for forgiveness. Borrowers with mortgage interest, rent, or utilities expenses must have claimed (or be entitled to claim) these expenses as a deduction on their 2019 Form 1040 Schedule C in order for these expenses to be eligible for forgiveness.

- Partnerships: Borrowers who are general partners in a partnership are eligible to claim the same level of compensation as they were making as partner compensation when they applied for the PPP. Partner compensation is capped at the 2019 Schedule K-1 net earnings from self-employment (reduced by claimed section 179 expense deduction, unreimbursed partnership expenses, and depletion from oil and gas properties), all multiplied by 0.9235.

- Non-Payroll Expenses: All eligible non-payroll expenses must be paid during the Covered Period (not the Alternative Payroll Covered Period) OR incurred and paid on or before the next regular billing date, even if the billing date is after the Covered Period.

- $100,000 Limit: Be aware that if you pay any single employee (including yourself) more than $3,846.15 per 2 week pay period (an annualized $100,000 per year) that amount will not count towards the loan forgiveness. At time of this posting, the SBA has been vague about the exact way ineligible pay is deducted from the forgiveness amount, so, for best results, be conservative

If your loan is NOT forgiven

Your loan may not be approved for forgiveness or you may decide not to ask for forgiveness because you do not meet the forgiveness requirements. In this case, you will begin to make your principal and interest payments after the Deferral Period until the loan is paid off.

Ineligible Borrowers

The SBA has stated they will be reviewing ALL loans above $2 million and will sample the rest. Thus, it is highly recommended if you do NOT meet the PPP requirements that you contact Carson Community Bank to pay off your loan immediately. While not an exhaustive list, borrowers who meet any of the following criteria are those who may not qualify for PPP loans and should consult with their legal and financial professionals to consider repaying their PPP loan. For further information, consult 13 CFR 120.110.

- Borrowers who knowingly provided false information during their application process

- Financial businesses primarily engaged in lending or life insurance (e.g., banks and credit unions)

- Businesses headquartered outside of the U.S. or owned by undocumented aliens

- Businesses involved in any illegal activity

- Businesses involved with pyramid sales distribution plans

- Businesses that derive more than one-third of their gross annual revenue from legal gambling

- Private clubs and businesses which limit the number of members for reasons other than capacity

- Businesses with an owner or partner who is incarcerated, on probation, parole or who have been indicted for a felony or crime of moral turpitude